What to Do about CBDCs

What to Do about CBDCs

Get Yourself Ahead by Looking Forward

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts. Their massive overhead costs make micropayments impossible.”

- Satoshi Nakamoto

Hello Anons,

The last two posts on here have been thrilling. I think we understand what is happening in the world and the direction we are going. I believe this subject is too important to not stay up to date on. Pretty soon we are all going to hear the term CBDC regularly. It is my opinion the best thing we can all do is learn what is needed to keep us ahead of the game. That is what I am here for and what I will do for you. This post is going to involve an integration into cryptocurrency and what they provide for you in a future involving CBDCs. We are approaching that future faster and faster.

Quick Coverage on The FED and ECB

The US FED

The FED is reported to release their “paper” on a United States CBDC, seemingly to be called the “Digital Dollar”, this quarter. It would be very interesting to have a solid statement from the FED about what their goal is.

Their notions on it recently have been mixed. Some officials are hesitant about a “Digital Dollar”. The regulatory and legal framework involved to implement and launch this project is incredibly complex. It is understandable that FED Chair Jerome Powell is careful with his word choice and is slowly unraveling the FED’s stance on the subject leading into their “paper” or official statement. They have been working toward this for many years, so don’t be sold on the narrative that it isn’t an “important project” at the moment.

Just last year they started making more public announcements on their project for this. In August 2020 the FED starting releasing papers on their CBDC projects. An Update on Digital Currencies Remarks by Lael Brainard, Member Board of Governors of the Federal Reserve System:

“To enhance the Federal Reserve’s understanding of digital currencies, the Federal Reserve Bank of Boston is collaborating with researchers at the Massachusetts Institute of Technology in a multiyear effort to build and test a hypothetical digital currency oriented to central bank uses. The research project will explore the use of existing and new technologies as needed. Lessons from this collaboration will be published, and any codebase that is developed through this effort will be offered as open-source software for anyone to use for experimentation.”

This past February Powell called the Digital Dollar a “priority project”. They have been been experimenting with many different versions of a digital dollar. They’re adapting to the “cashless society”.

Andrew Ackerman released a segment on WSJ just on Oct. 4 covering the pending statements to come from the FED on how they plan to issue the CBDC in the coming weeks.

The ECB

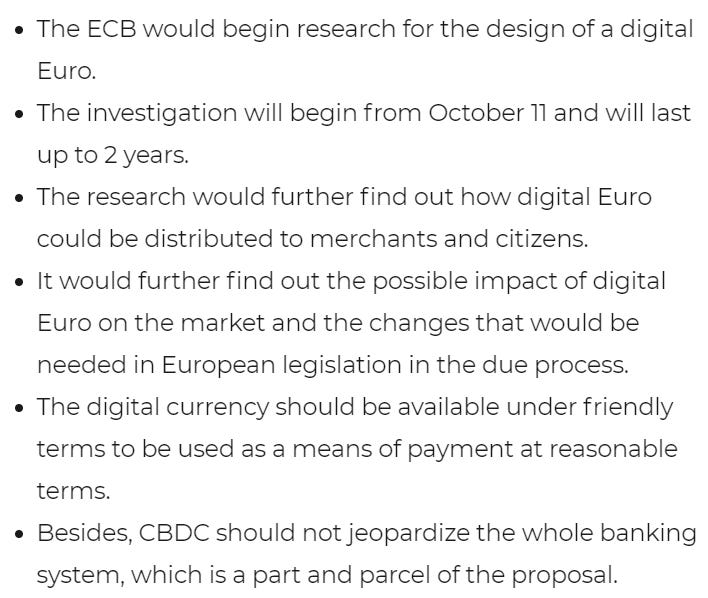

Just last month, the President of the European Central Bank, Christine Lagarde officially announced the beginning of a 2 year investigation into developing the Digital Euro. Bitcoin.com reports that the ECB “believes to be prepared with the technology ready to respond and meet people’s demand of a CBDC in the EU with the Digital Euro.” Lagarde interviewed with Klaus Schwab, Founder of the World Economic Forum (WEF), and laid out the plans for the Digital Euro:

Broad CBDC Overview

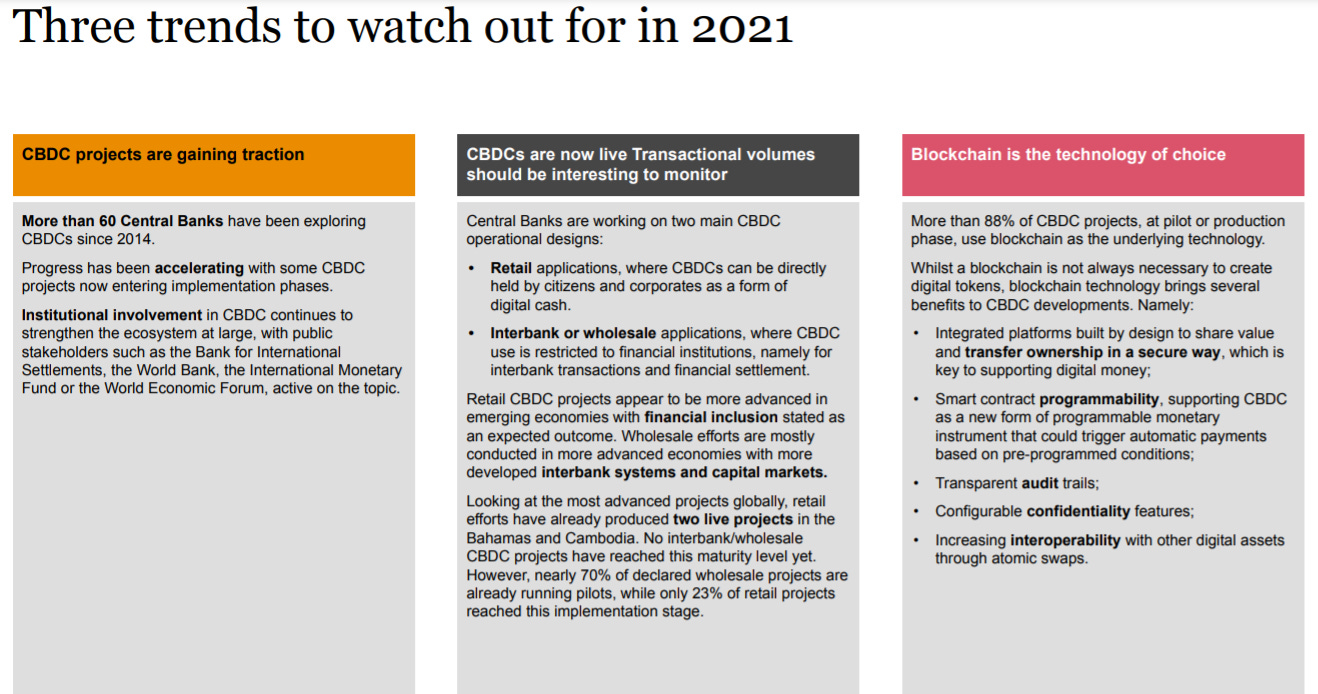

Moving forward with general CBDC information, I would like to highlight a recent publication from PwC, Member of the BIG 4 accounting firms, covering CBDCs on a global scale.

There is a lot packed into this one graphic, still, it boils everything down to the common themes I have been reading on this.

Retail CBDCs aim to improve “financial inclusion”, bringing this to the unbanked is a primary focus.

The two CBDCs that are up and running are Retail CBDCs (Bahamas & Cambodia). Retail CBDCs are in more advanced stages of production than Wholesale CBDCs.

There aren’t any wholesale CBDC projects that have reached gone “live” yet. Nonetheless, nearly 70% of the wholesale CBDC projects are already running pilots, and only 23% of retail projects reached this implementation stage.

More than 60 Central Banks have been researching CBDCs since 2014.

Public stakeholders such as the Bank for International Settlements, the World Bank, the International Monetary Fund or the World Economic Forum, are active on the topic of CBDCs.

88% of all CBDCs in the production or pilot phase use blockchain.

Implications for You

If there’s anything that is creating resistance and hesitation in the “retail” market, it is the lack of privacy that is coming from the launches of CBDCs. Coming from the FED and EU, there seems to be a lot of desire for more oversight.

The most recent example of this fear comes from the US. Treasury Secretary Janet Yellen recently backed and supported Biden’s expanse of the IRS and the tracking of all banking transactions. Yellen’s supporting claim for the reason behind this proposal was “ the ‘enormous tax gap’ in the US as the reason behind the proposed tax hikes and information collecting, blaming the gap on places where information on income ‘can be hidden’.” Further noting, “It’s just a few pieces of information about individual bank accounts, nothing at the transaction level that would violate privacy,” Yellen said.

Big Takeaway: Under the proposal, banks would be required to turn over aggregate inflow and outflow numbers annually to the IRS and would cover bank accounts with at least $600 or at least $600 worth of transactions, according to the Wall Street Journal.

We all know the advent of cryptocurrencies lead to this central banking adoption. There’s no shortage of oversight desire coming from big government. The lack of privacy and lack of control is what makes a CBDC undesirable. No matter how we feel about it, they are coming this decade. It is going to be a fundamental change and will have massive implications on you.

Some of these disadvantages I covered in the last post. There’s a lot of speculation involved in trying to anticipate the negative features, the bottom line comes to knowing what you can do to put yourself ahead.

If you, the reader, aren’t educating yourself on crypto you absolutely have to. This is the future. There’s so much to know about the subject and why there is such a massive demand for it.

To start, I’d like to quickly cover what Bitcoin is to give you an idea as to why it’s important for you, and your future.

BITCOIN (BTC)

Bitcoin Whitepaper (Click to read)

Bitcoin is a decentralized peer-to-peer (P2P) electronic currency with a long-term finite supply.

How does it work?

Bitcoin is decentralized, meaning not in one *central* place. All of the node operators, miners, and users, all of it is decentralized. The operations are distributed globally without a central means of power or authority.

The Bitcoin Blockchain is a chronological public record of transactions saved in time, and shared by all bitcoin users. This public ledger secures the history and ongoing use by verifying all transactions to prevent *double spending*

Bitcoin utilizes public key cryptography, proof of work, and peer-to-peer networks. Public Key Cryptography is what secures everything using mathematics. It is used to prevent anyone fund spending another user's bitcoin and accessing their wallet. Simply put, it uses a pair of keys, public and private keys and it is impossible to derive your private keys from your public keys. There is a big difference between public keys and private keys.

Your bitcoin private key is generated in random when you first start using your wallet. It is a sequence of numbers and letters, which enable funds to be spent whenever you want to send a transaction. This private key is impossible to reverse because of the incredibly strong encryption code base within the Bitcoin protocol. A bitcoin private key will always remain mathematically related to the specified user and their bitcoin wallet address. The public key is connected to the public address generated to receive BTC. It is seen by everyone. It is made up of, also, a long sequence (hash) that is compressed and shortened to generate the Bitcoin payment address.

The “wallet” is a device that stores your private keys and enables you to send your coins. It contains the necessary information to access your BTC. It contains the “keys” to your coins, your private keys. These “sign” or produce “cryptographic signatures” to send BTC to another address.

The idea of a wallet can be confusing. It doesn’t directly download your coins. You’re not sending them into the wallet. It is used to *access*.

Since it is a peer-to-peer (P2P) electronic currency, BTC are sent/released from the *senders bitcoin address* to the *receivers bitcoin address*. Each Bitcoin user can/should have multiple Bitcoin addresses.

***Your bitcoin address is the ONLY information someone needs to pay you in BTC***

If you plan to purchase Bitcoin and want to be *smart* and secure your assets, you *must* purchase a wallet. Start with a Trezor or a Ledger, or, if you really want the best for security., a ColdCard from CoinKite (BTC only).

Links for the 3 are listed as follows:

Ledger → I recommend the Ledger Nano X

Trezor → I recommend the Trezor Model T

ColdCard → (Bitcoin only). Highly secure and very technical. This should be used by people who are already familiar with hardware wallets. I recommend KISB Guide Bundle or Uncle Jim’s Bundle from CoinKite.

Note: You should have multiple wallets.

Quick Example: To make this entire thing translatable, I will use email as an example: You can send and receive from *multiple* email addresses. Each address used for different purposes, it wouldn’t make sense to have ALL your emails coming and going from one address. It wouldn’t be an efficient or effective use of its purposes. Additionally, most people will use multiple email addresses for privacy and organizational purposes.

How is it Valuable?

1. Features

Bitcoin is a peer-to-peer (P2P) electronic currency with a finite supply. More importantly, it brings autonomy (sovereignty) to the individual over the legacy financial system. You are operating outside of the banks, and you are becoming your own bank.

It is *permission less and borderless*. Anyone can use it if they want.

It is *censorship resistant*. Nobody can freeze or prevent anyone from sending a transaction.

It is FAST. No waiting for intermediaries. Also, the transactions on the 2nd layer Lightning Network can move at the speed of light. On the base layer they can move slower but are being scaled out now with the ongoing development of the 2nd Layer with lightning transactions.

It is cheap, fees are low to send BTC.

Storage - highly secure and very minimal. Takes up no space. Easy to hide wallet.

No counterparty risk. Once you store your keys and wallet intelligently (more on this later) and your transaction is confirmed, you are set!

2. Monetary Value

It is scarce. The supply now is at ~19 million bitcoins. There are only ~10% left to be mined. There are only ever going to be 21 Million bitcoin (unlike gold or the dollar). This issuance schedule which is reduced every 4 years from the Halving Cycle. Every 4 years, the amount of Bitcoin produced is cut in half. This cuts the amount issued per block in half. We are now at 6.125 BTC per block. Next halving is in 2024.

*This means it is literally programmed to be scarce.*

There is only ever going to be a certain amount. Long term holders and new holders continue to move their BTC off the exchanges, into their personal wallets, and holding. You can see that now on the centralized exchanges like Binance where they are changing the amount you can withdraw. This screams supply and demand.

It is a store of value. Bitcoin cannot be printed or debased (see -US Dollar). Think of the bond market right now, currently the *negative yielding*. People are parking their money here and losing it. Bitcoin’s store of value characteristics should play as a competition to this once people start thinking.

Bitcoin market cap is right under $1T currently. Think that there may be a small chance that money flows into here from negative yielding bonds, alone?

Institutions are also buying this asset as a hedge against inflation. High Net Worth clients at large banks want this asset. Our generation prefers this as they support the ongoing “wave of dematerialization” that is occurring.

Necessary Mental Framework

“ Okay, I understand that….But I see the price of this moving all the time. Wasn’t it just at ~$65K? I would’ve lost money!!”

***1 BTC = 1 BTC***

You will need to understand that and wrap your head around that from this point forward. Think long and hard about this….

To help you understand so this makes sense -> The USD “price action”, AKA – day-to-day price movement, isn’t something to focus on. 1 BTC is 1 BTC.

Again, this was covered last time, but I think it is important to revisit.

This is NOT about making more USD. You absolutely don’t want to be caught up thinking in terms of “the tip of the iceberg”. You want to make more USD to buy more assets. Buying BTC or AAPL shares to earn more USD is thinking small.

You are taking part and getting involved in revolutionary changes in finance and technology. This is much bigger than trading for fiat diluted dollars.

When I have the ability to transact in a currency that cannot be diluted and debased in a matter of a few electronic entries on a central bank’s balance sheet, it is fully backed by code, and I can take it anywhere I want, use it, transact with it 24/7. All knowing that it is programmed to be scarce…why wouldn’t I?

If you have any questions or comments please share!

Disclaimer: None of this is to be deemed legal or financial advice.