Welcome to CBDC Watch

Welcome to CBDC Watch

Echoes of a CBDC from Our Past and Into Our Future

Introduction

The Times 03/Jan/2009 Chancellor on brink of second bailout for banks

This message right here should set the tone for this entire substack and future publications. If you ever want to understand what is happening→ that message, date, author, and provenance will tell you everything.

We have developments on CBDC’s occurring on a large scale. This is a digital token issued by a central bank as a response to the massive developments in cryptocurrencies. Bitcoin, the first cryptocurrency, and CBDC’s, central bank issued tokens, are direct opposites of each other. I can say with 100% certainty the implications of this will bring forward an erosion of privacy unlike anything we’ve ever seen.

I am fully vested and believe it is critical to be on the forefront of this. This is going to have cascading changes on your life.

To begin, we are going to provide some historical context for you as a way to bring you all up to speed. For this, we are going to cover the European Central Bank.

The Root of All Fuckery

ECB Historical Context and Overview by BowTiedFellow.btc

For those of us who are familiar with Raoul Pal, a former hedge fund manager and founder of Real Vision, we are aware of CBDCs (Central Bank Digital Currencies) lurking in the background. For those of us who are familiar with the Central Bank Cartel, we understand the global human suffering, alarming wealth inequality, and power transfers that have resulted from fiat currencies issued by Central Banks.

It would behoove anyone reading this post to familiarize yourself first with Raoul’s breakdown of CBDCs in this Twitter thread posted below:

Some key takeaways from the thread: The advent of CBDCs give Central Banks the ability to circumvent governments in the implementation of monetary and fiscal policy, and would give Central Banks the ability to control human behavior through their use of big data analytics and “behavioral economics” to incentivize things such as eating bugs (See how this is starting here WEF) or limiting the end-user’s carbon footprint.

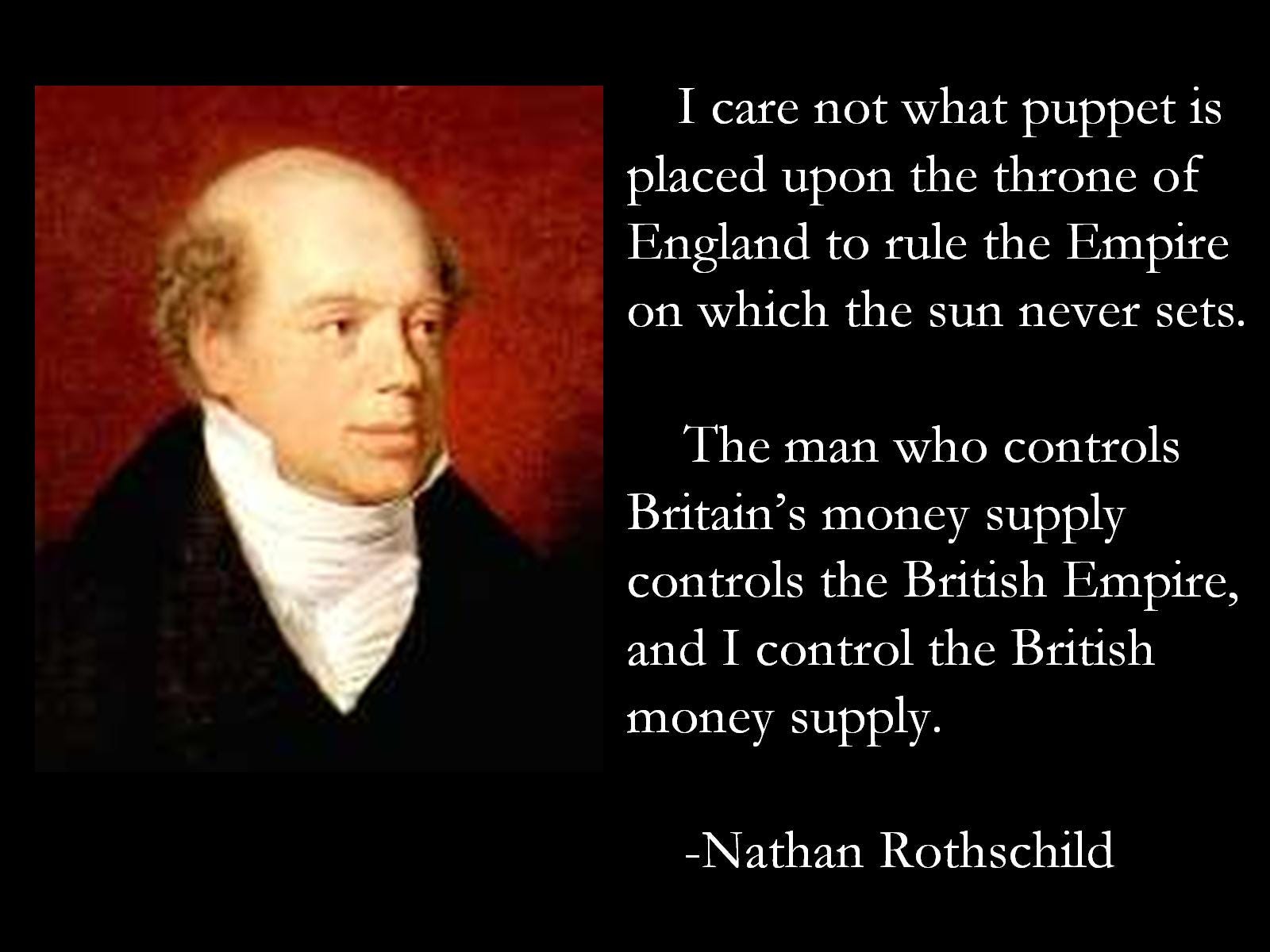

Additionally, here is a brief summarization of the motives of the Central Bank Cartel provided by none-other-than Nathan Mayer Rothschild, the infamous 19th century banker and financier to whom German poet Heinrich Heine declared “money is the God of our time and Rothschild is his prophet”:

Context on the Banking Apparatus

Nathan Rothschild’s self-admission that the authority of the banking apparatus to control the money supply of a nation undermines that nation’s ability to govern outside the sphere of authority of the banking apparatus. This may be taken to it’s next logical conclusion in that their intention is to undermine the citizenry of all nations within their sphere of authority. A nation’s dependence on the banking apparatus may yield an embracement of extremely unpopular policy positions because it serves the interests of the banking apparatus, contrary to the interests of the citizenry.

There exists a fine line for the banking apparatus to tread, based on their general awareness of the citizenry’s desire for self-rule. Revolts against governments blatantly violating their social contract with the citizenry have resulted numerous times throughout history. In which these revolts are labeled as “peasant revolts”, a gentle reminder by the banking apparatus of where the citizenry stands in the pecking order.

To further their own interests while avoiding the potentiality of a revolt, the banking apparatus must roll out their policies in a calculated manner to ensure they are accepted by the general populace. Which is to say the policies must convince the citizenry that the policy in question is in the best interest of the citizenry. The manner in which the banking apparatus may attempt to seize authority over a citizenry is determined by the amount of resistance to the seizure they may expect. If that resistance is expected and may be subdued, attempts will be made to do so, and if it may not be subdued, arrangements will be made for future attempts.

Multilateralism is an alliance of multiple countries pursuing a common goal. Its gradual implementation over the past century has led to the creation of an extraordinarily complex international monetary network. This network outsources policy solutions from various international institutions backed by prominent stakeholders of the global banking apparatus. Multilateralism is a backlash to unilateralism, perhaps because the idea of a nation acting within their own interests in the international arena is repugnant to the banking apparatus.

The overarching themes of multilateralism, which are international unity and cooperation, conveniently run parallel to the interests of most nations. Unbeknownst to them, the policy positions pushed are simply an effort to standardize the citizenry of these nations at the expense of their individuality, and then to that extent, standardize all nations.

When a citizenry is standardized, their previous identity is rendered null and void (Brexit is a good example here), and to that logical end, any association with that previous identity may be considered outside the boundaries of the newly established acceptable social standards and norms. Standardizing the citizenry of a nation would isolate the elements resistant to change and leave them more susceptible to being targeted in this top-down policy implementation effort. This may be conducted as many times as necessary until any resistance from the citizenry is rendered futile and the nation effectively serves the interests of the banking apparatus. Once all nations within the sphere of authority of the banking apparatus effectively serve the interests of the banking apparatus, the previous identity of the nation is similarly rendered null and void and resistance to change would leave individual nations susceptible to intentional destabilization until submission.

Multilateralism and the European Union

While the United States of America has the Declaration of Independence, the Bill of Rights, and U.S. Constitution seemingly serving as the foundation for its governance, the European Union is the end-product of the Lisbon Treaty reforming the Maastricht Treaty into the Treaty on European Union and the Treaty of Rome and into the Treaty on the Functioning of the European Union, after the Treaty of Nice also amended the Maastricht Treaty and the Treaty of Rome to accommodate eastward expansion after the Maastricht Treaty formally integrated member-states within the European Communities formed by the Merger Treaty that *partially merged* the Treaty of Paris, establishing the European Coal and Steel Community, the Treaty of Rome, establishing the European Economic Community, and the Euratom Treaty, established the European Atomic Energy Community.

The European Union, under all its multi-level governance complexity, is the brainchild of the banking apparatus that seeks to use multilateral governance to undermine the national identity and sovereignty of its member-states. The integration of the continent of Europe has long been hypothesized and its execution fancied by the likes of self-proclaimed elitist Richard von Coudenhove-Kalergi. He envisioned an ethnically heterogeneous Pan-Europa (which begs the question - is the pursuit of homogenizing all ethnicities into one a form of ethnic cleansing?), and Winston Churchill, a globalist darling, in his call for a “United States of Europe”.

Even after the establishment of the European Union by the Maastricht Treaty, there still existed a strong push for a more transnational elitist European Superstate which would consist of an EU foreign minister and foreign policy, an EU defense policy in addition to or separate of NATO, a European Justice System with a common asylum and immigration policy, and the supersession of laws within member-states to EU law. Even those subservient to the interests of the central planners feared this would subject nations to the very same subservience the nations were in fact already subjecting their citizenry to, and the plan for this European Constitution was scrapped, until there existed a push for the Lisbon Treaty. The only difference between the originally proposed Constitution and the Lisbon Treaty was a matter of approach rather than content whereby the Constitution was simply broken into pieces and the pieces amended onto already existing treaties. Although not quite as clear-cut as the original Constitution, the Lisbon Treaty implemented mechanics that would yield similar results for circumnavigating national sovereignty, though it would be through the approach of complex multi-level governance rather than direct ascension.

In a Factsheet published on June 24th, 2021, titled “EU Agenda For a Renewed Multilateralism”, the European Commission lays out the groundwork for the European Union’s renewed multilateral agenda:

There is a bizarre irony in their declaration of multilateralism as an effective and efficient means of governance when the entire working theory behind European integration is through a “failing forward” process, where incomplete policy solutions should lead to policy failure, leading to further reform and deeper integration. But considering this ineffective or inefficient couldn’t be further from the truth. In the pursuit of this strategy, when using multilateralism to serve the interests of the banking apparatus, the actual failure from said policy failure would be letting a crisis resulting from the policy failure go to waste.

In that regard, every policy failure serves a deeper purpose of further integrating Europe into the interests of the banking apparatus. Considering the European Commission’s declaration that the European Union desires to further serve global interests and values under one voice, one must wonder who’s voice they are referring to, why policies are being implemented that are intentionally incomplete, and to what end the failure of existing policies may lead.

Enter the European Central Bank

Similar to how there have been strong desires throughout the last century among the central planners for a greater Europe unification, so too has there existed the idea of for a single European currency. The idea was originally proposed to the League of Nations and again in the 1950’s at a European Forum in which it was argued by De Nederlandsche Bank Governor Marius Holtrop that unifying Europe may be possible under a common central bank policy. It was largely determined that the integration of member-states within Europe into a greater Europe would be most feasible if the economies of the member-states were converged together.

The European Central Bank, established in 1998 and headquartered in Frankfurt, Germany, is the central bank of the Eurozone. It is preceded by the European Monetary Institute, which was created a few years earlier with the intention of laying the foundation for the Euro and the European Central Bank. Further preceding the European Monetary Institute is the European Monetary Cooperation Fund, which was established by the European Economic Community and tasked with intervening in the exchange market for European Community member-state currencies to reduce fluctuation between the currencies and coordinate policy on settlements between the Central Banks.

The decision-making body for the European Monetary Cooperation Fund was the Board of Governors and was made up of governors from the central banks of European Economic Community member-states. The European Monetary Institute was also staffed by predominantly members from these central banks. This European monetary cooperation began in the 1970’s with the intention of pegging all the currencies within the European Economic Community. Essentially, the central banks within each European Economic Community member-states lobbied for multinational agreements under the guise of greater monetary cooperation, which yielded the banking apparatus multinational monetary oversight that said member-states were subjected to.

After USD was removed from the gold standard, European monetary cooperation called for pegging the currencies of the European Economic Community together. This cooperation is deemed the “snake in the tunnel”, whereas the European Unit of Account (EUA) and then the European Currency Unit (ECU) attempted to provide a band (tunnel) for currencies to trade within. These units did not override the value of national currencies, yet economic shocks and the tendency for currencies to trade opposite ends of the tunnel (currency A appreciates while currency B depreciates) ended with the tunnel collapsing.

However, this was far from a failure. The ECU was always a means to an end, and the end was always a unit of account that would override the value of national currencies (implemented as a store of value and medium of exchange). Economic hardships, such as unemployment and slowed economic growth, led to a polarization between nation states seeking further integration with each other and nation states skeptical of the European monetary cooperation. Many sought for expansionary monetary initiatives, which utilize political language aimed at justifying the act of expanding the money supply, while others sought for price stability, which was known to be an impossible objective in a world where Keynesian Economics is the dominant school of economic thought. Both solutions would lead to further economic hardships in which further monetary cooperation always coincidentally appeared to be the solution most publicly unchallenged.

European Monetary Institute was formally replaced with the European Central Bank, who sought as its primary mandate to maintain price stability with its issuance of the Euro, which it was able to successfully implement in mostly all the nation states within the Eurozone. It was not even a decade of the Euro existing before the ECB’s secondary mandate began showing its dominance. Stated within the secondary mandate, the ECB (or rather, the ESCB, which also encompasses the Central Banks of the European nation states who have not adopted the Euro as their native currency) shall “support the general economic policies in the Union with a view to contributing to the achievement of the objectives of the Union…”

Essentially, the secondary mandate enabled more expansionary monetary initiatives. One of initiatives, or tasks, that is justified is the issuance of banknotes, which the ECB holds the exclusive right to authorize. Now extrapolating over to general monetary phenomena, the issuance of banknotes has always been the answer to how to stimulate the growth of a domestic economy. It is understood as boosting consumer spending and increasing capital investment, but many know it truthfully to be an invisible tax on the people. Immediately following the Great Recession, the ECB was faced with handling a years-long Eurozone debt crisis, to which they responded they would do “whatever it takes” to preserve the Euro, even against the wishes of nation states who were too entrenched in the monetary “cooperation” to bail out.

The actions that followed created consequential precedents that justified their adoption as levers a central bank may regularly pull to handle economic crises. These levers range from bank bailouts to quantitative easing and all the way to the grand finale of direct debt monetization. With debt monetization being the practice of a government borrowing from a central bank for the purpose of financing public spending, quantitative easing is a form of indirect debt monetization where this practice of money creation is ferociously defended. Quantitative easing is now conveniently accepted as a means of stimulating the economy, but is failing to do so in the current macroenvironment.

The COVID-19 crisis has led to governments globally increasing their public spending to support households and businesses, but failing to sufficiently raise the revenue required for doing so. The deficits that have resulted from this are financed by central banks who purchase their debt, with some governments getting a pass on over-drafting (could citizens get away with that?). Governments are now heavily reliant on central banks for public spending and the line between monetary and fiscal policy is essentially eroded. The people of a nation state rely on their government and their government is now fully reliant on their central bank. The words of Nathan Rothschild have never rung more true and the way is now paved for an even more sinister form of monetary control.

The CBDC Series

Enter Central Bank Digital Currency

An Introduction to the CBDC Series by BowTiedScholar

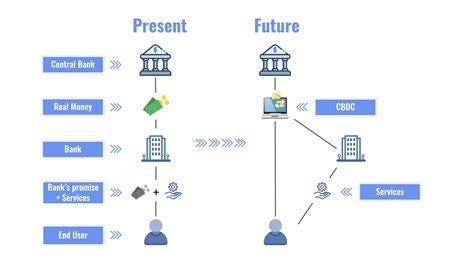

A central bank digital currency is a digital/virtual central bank version of the already existing currency, $1 of CBDC is worth the same as a $1 bill or $1 in a bank account. In this case fiat money ($USD, $EURO). They are “pegged” to those currencies on a 1:1 ratio so they maintain their equivalence in spending power.

Up until very recently the idea of this was thought to be “crazy” by the general public, but not so crazy by the “makers”. The idea was generally accepted, but held in question until recently. They had no idea how mature the technology is, were generally focused on how effective it would be, and were unsure of the implications of such a large scale change. Now, today we have more than *leaped* into this reality by a large measure.

There is an all out race to the finish to implement these CBDC’s now.

The ECB estimates that upwards of ~80% of central banks are exploring this form of currency. To date, two central banks are now live and numerous others are in late-stage pilots. Bahamas and Cambodia are now live with their CBDC running and fully operational. Both, ironically, have their currencies and transactions backed by the USD…heads up Federal Reserve.

China launched it’s pilot of their digital currency/electronic payment (DC/EP) and have with it: 113,000 consumer digital wallets and 8,859 corporate digital wallets that were opened between April 2020 and August 2020. During that short time, both consumer and institutional/corporate users exchanged, in USD terms, $162 million across 3.1 million digital yuan transactions. The bank also uncovered *almost 7,000 use cases*. As well as banning cryptocurrency mining operations and transactions.

The Bank of Japan has already began testing it’s CBDC and expects to roll out a trial run of it in the near future. Keep your eyes open for that.

The EU and their CBDC → Back in Nov 2020, the EU was in the beginning stages of their “experimentation” phase of a CBDC. Not so much at this stage, they’re in the early stages and agenda setting stages.

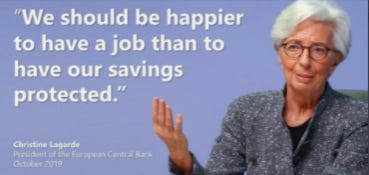

Christine Lagarde continues to be dismissive of cryptocurrency, as we all know. Seeing as they have *coincidentally* sped up their pace on a central bank digital currency. Fast forward to today and the “Digital Euro” and the ECB claim to offer more “privacy and protection”. ECB Board member, Fabio Panetta, who criticized the profit-making agenda of private stablecoin issuers is not soft spoken on this agenda.

“the CBDC is a digital instrument: it is easily scalable and has no storage costs, unlike a physical instrument like cash. The CBDC is also a hybrid instrument: it is both a means of payment and a financial asset. The CBDC is a safe asset: it is not subject to duration risk, unlike bonds, or to risks of bank runs & limited deposit insurance, unlike commercial bank deposits, or to inflation risks when it is remunerated" - ECB

They feel the pressure and threat of cryptocurrency. We now have the complete and total opportunity to financially operate on our own. (Looking at you Lagarde)

The Characteristics

Now that you realize that the implications of CBDC’s are much larger for *YOU* than they are for them. These same CBDC’s are going to be subject to the SAME existing disadvantages these currencies already possess.

Policy

Central Banks (The Federal Reserve/The European Central Bank) print money and print money, and then print some more “money”. Mostly achieved through a *monetary policy* called “Quantitative Easing” where the central bank puts an electronic entry into their balance sheet in CASH and they use that “money” to purchase long term government bonds. The government creates new money to purchase bonds.

“Economists”, a synonym for ZEROS, will try to argue that it is an “asset swap” and argue that it is *money supply expansion* and not “printing money”. Comically they walk themselves into a dead end here, because do either of those sound good to you, and does that argument make any sense? (Check - inflation).

Pegging

$1 of CBDC is worth the same as a $1 bill or $1 in a bank account. In this case fiat money ($USD, $EURO). They are “pegged” to those currencies on a 1:1 ratio so they maintain their equivalence in spending power. The expansion of the money supply is *endless* and it creates a bigger hurdle as time goes on. Your salary is not going up at the rate of inflation → saving money becomes harder and harder as this continues. Prices of goods and services are rising, taxes are rising, asset prices are rising. Long term, this gets worse and worse.

The larger Central Banks of the world are now beginning to test to prepare for a release of their CBDC’s for official launch. This comes with *many* strings attached to it.

Chart from the ECB describing the advantages of their CBDC

Privacy

These are going to assert a lot of control and come with a loss of privacy. The data, behaviors, your locations, sending and receiving, everything is going to be directly stored and saved and sent to the central bank.

Interchangeable

CBDC is an equivalent in value to the nation’s existing currency. I can be exchanged for other currencies, redeemed, or “bought” for equal amounts. The movement and process will involved less friction

Digital

This is obvious, I know. It is a worthy feature, but of course anything digital needs electricity and network connectivity in some way.

P2P

The idea for this is that we will be able to transact outside of financial intermediaries with each other. They want to create convenience and a seamless process for this.

Programming

As CBDC use cases grow and develop, their definition will adapt as needed. It is certain that each nation’s CBDC instantiation will differ as they adapt to unique economic needs. As such, additional characteristics will continue to emerge and be categorized as either required, but not sufficient or as desired, but not required.

They will be able to program and update this any way they need to. It will come with consequences. Think things like public access, welfare recipients, social/credit scores, criminal history, travel bans, transportation, etc. This is going to go very far and deep.

Cryptocurrency is the freedom and self-sovereign enhancing financial technology they fear.

Moving Forward

The CBDC Series will have weekly postings updating you and covering more details on the digital wallets, differences in all CBDC’s by central bank and category.

I will have a lot to cover on this going forward. Stay tuned!

Conclusion

Thank you to BowTiedFellow.btc for the assistance and partnership. It was a pleasure working alongside someone with so much knowledge, and the number one resource I know when it comes to BTC, STX, and MIA.

I know this was a long one. Thank you very much for reading. If you enjoyed and are interested in next week’s posting, subscribe and share with your friends.

Fantastic post gents, subbed!