Life with a CBDC

CBDCs Affecting Your Day-to-Day

Hello all, BowTiedScholar here. I’ve been covering CBDCs for some time on CBDC Watch and crypto news for BowTiedIsland. This is an in depth look on CBDCs and their implications on you.

Coverage on CBDCs

We’ll be covering retail CBDCs with an emphasis on the Sand Dollar and the Digital Yuan. These are two of the most significant CBDCs in development. Both launched their current phase of operations in 2020, with the Sand Dollar already fully operational and the Digital Yuan gradually proceeding in the pilot phase.

Both CBDCs run off account based systems providing applications and platforms to interact directly with the Central Bank. Meaning they’re not tokenized and have no capacity for anonymity.

The Sand Dollar

It all started with the Bahamian Sand Dollar, the world’s first live Retail CBDC. A quick timeline on it’s development. The Central Bank of the Bahamas (CBoB) started developing the Sand Dollar in partnership with the International Monetary Fund (IMF) and their tech partner, NZIA Limited. Here is a video from the Central Bank of the Bahamas and the IMF selling adoption of the CBDC.

The reason for developing the CBDC was increasing financial inclusion with an emphasis on innovating financial services through digitalization. Fast forward to the retail CBDC pilot in 2019. The pilot started on the island of Exuma on Dec 27, 2019 and after some quick success the pilot expanded to the island of Abaco on Feb 28, 2020.

Testing on these islands was based on configuration of each representing the general layout of the Bahamas. After the success with the pilot program the Sand Dollar launched nationally on Oct 20, 2020.

The Central Bank of the Bahamas uses a hybrid model for their technological design of the Sand Dollar. A centralized ledger to record transactions and uses DLT for end of day records.

The Sand Dollar is designed through a two-tier system, thus being fully intermediated. This means the financial institutions have an interoperable platform and are all connected to the Sand Dollar Network and it provides the users the ability to convert into the CBDC. Intermediation impacts the distribution of the Sand Dollar. Thus the rollout to the financial institutions has been a gradual process through Authorized Financial Institutions (AFIs).

Their objective for the CBDC was eliminating obstacles to financial access, otherwise known as “financial inclusion” after COVID and Hurricane Dorian sped up digital adoption. Establishing interoperability among financial services platforms, and stressing the need for KYC in the name of increasing security and safety in payments and “limiting illicit finance and money laundering” as a motivation. Tracking their citizens has been a large focus for this. you can find “disincentives” posted on the website for using and holding cash.

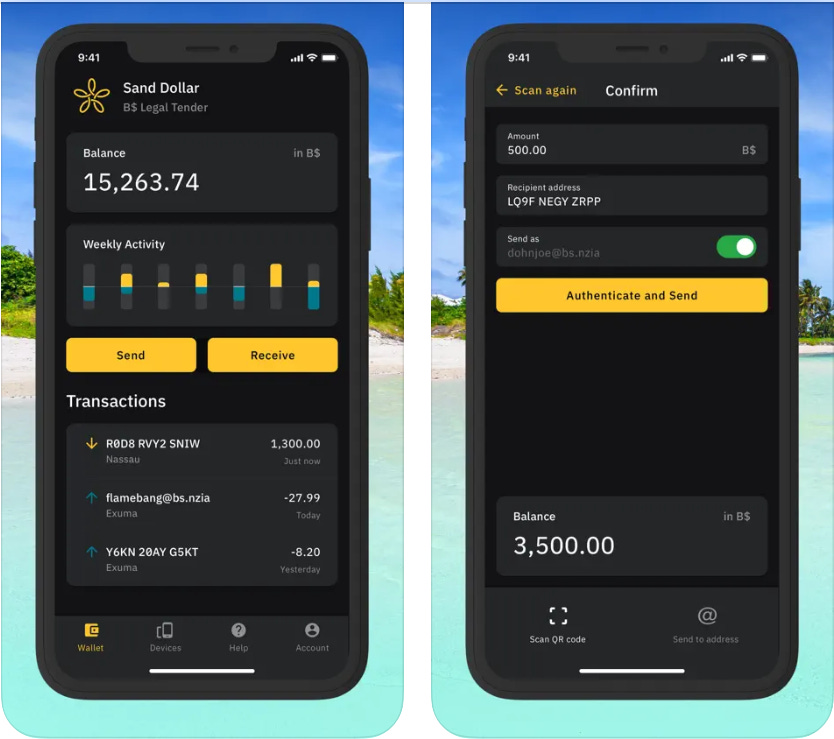

The Sand Dollar is used and accessed via the Sand Dollar App for both iOS and Android devices. CBDC applications in many ways are similar to Apply Pay.

Transacting with the Sand Dollar comes with zero transaction fees/costs for individuals. To pay users simply scan a QR to pay, and transactions are settled within a few seconds. Access to enroll comes with KYC through the user’s AFI.

The wallets are tiered into 2 different sets of users. Tier 1 is for small and unsubstantial users amounting to small payments. Limiting $500 of holdings and $1500 in monthly transactions. Tier 2 comes with $8000 holding limit and $10,000 in monthly transactions.

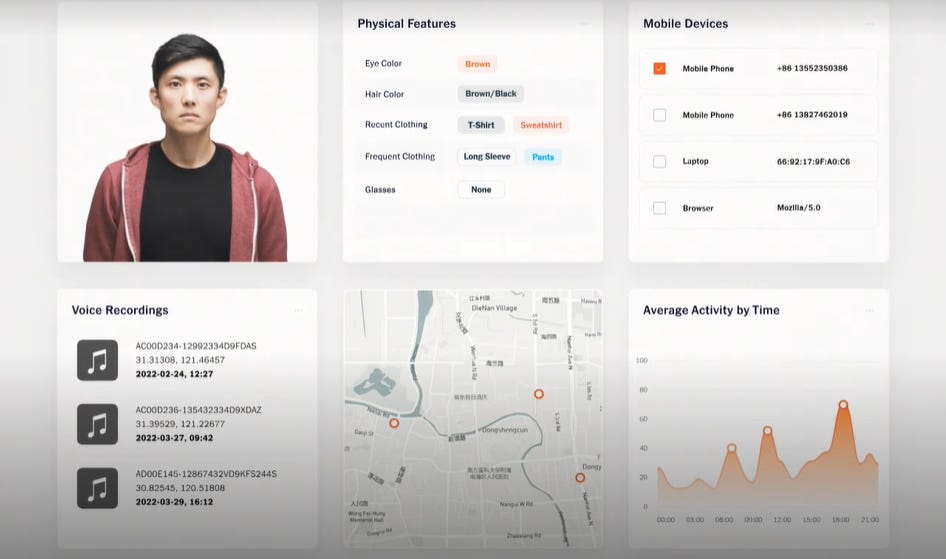

Features:

Biometric transaction authentication: Face ID, finger print/Touch ID

2 Factor Authentication via NZIA Authenticator (managed NZIA CBDC Security Keys) - Protected via Face ID and Touch ID

Transaction tracking

Geolocation tracking

Remote activation/deactivation to accounts and cards

Physical Card alternative

Digital ID Solutions

The facial recognition authentication is not limited to the Sand Dollar app, other AFIs have been compliant in this realm. Some of those being SunCash who partnered with PopID and PopPay to enable face ID authentication.

The Sand Dollar is currently used for domestic payments and micro-loans. It is currently accepted for retail transactions, Bahamas Registered Stock purchases, and Treasury Bills.

Digital Yuan (e-CNY)

As much of a big deal as the first ever CBDC, the e-CNY, Digital Yuan, e-RMB, DC/EP, all names for The People’s Bank of China’s CBDC. Why does it draw such a large focus? It is the first major retail CBDC to have successfully launched a major pilot in a major economy.

In 2016 the PBoC established the Institute of Digital Currency and created the first e-CNY prototype. By 2017 Ant Group began assisting the PBoC on the development of the Digital Yuan. Later that year the State approved and engaged in other institutions to develop and test the e-CNY. It was during this time Chinese officials began to notice a declining use in cash and a large transition toward digital payment services and identifying the need to adapt.

The PBoC initially launched the pilot program on the basis to innovate, improve efficiency, manage anonymity, increase security, create adaptive infrastructure, and increase financial inclusion. The internal testing phase for the Digital Yuan began in 2019 in Suzhou. After it’s success on a small scale, the first external pilot test began in April 2020. Unironically, exactly one year later the major cryptocurrency ban was executed and led to the Bitcoin miner exodus.

China uses a hybrid model for their technological design of the e-CNY. A centralized ledger to record transactions and also uses DLT for end of day records. The same model as the Sand Dollar.

The e-CNY, like the SandDollar, is intermediated and involves commercial bank intermediation. The pilot began with an airdrop, and has been the long standing primary method of distribution ever since. Thereby providing users with the option to convert into e-CNY as needed. Some of the banks involved in the pilots are the Bank of China, Agricultural Bank of China, Postal Savings Bank of China, ICBC, and more.

“Airdrops” have been a major contributor to the levels of adoption the e-CNY has seen since the beginning. Reassuring the PBoC on their plans to replace all cash and coin with the e-CNY over time.

The pilot currently is active in 28 major cities and 10 regions in China. Shenzhen has been a focus for testing, in addition to major cities like Beijing, Shanghai, and Guangzhou all being some of China’s largest cities (78 million across all 4 cities).

Wallet app adoption has seen a large increase since the initial release in April 2020. Up until June 2021 the number of personal wallets opened was low, only reaching approximately 21 million and 3.5 million corporate wallets, and by October there were 123 million wallets and over 9 million corporate wallets.

So far in 2022 the PBoC reports the e-CNY has reached 10,000 transactions per second (TPS) and currently over 261 million total wallets. That number is equivalent to 78% of the US population, or about the same as the total population of Spain, France, Germany, and the UK combined. Again, airdrops have been a massive incentive.

The e-CNY app, still in pilot, is being developed by the Institute of Digital Currency and is currently one of the fastest growing downloaded apps in China. e-CNY can be directly accessed via the app and by a physical hardware based electronic card manufactured by Chutian Dragon and IDEX. The hardware option also comes with offline payment capabilities with the long term plan for complete offline capabilities for individuals and businesses.

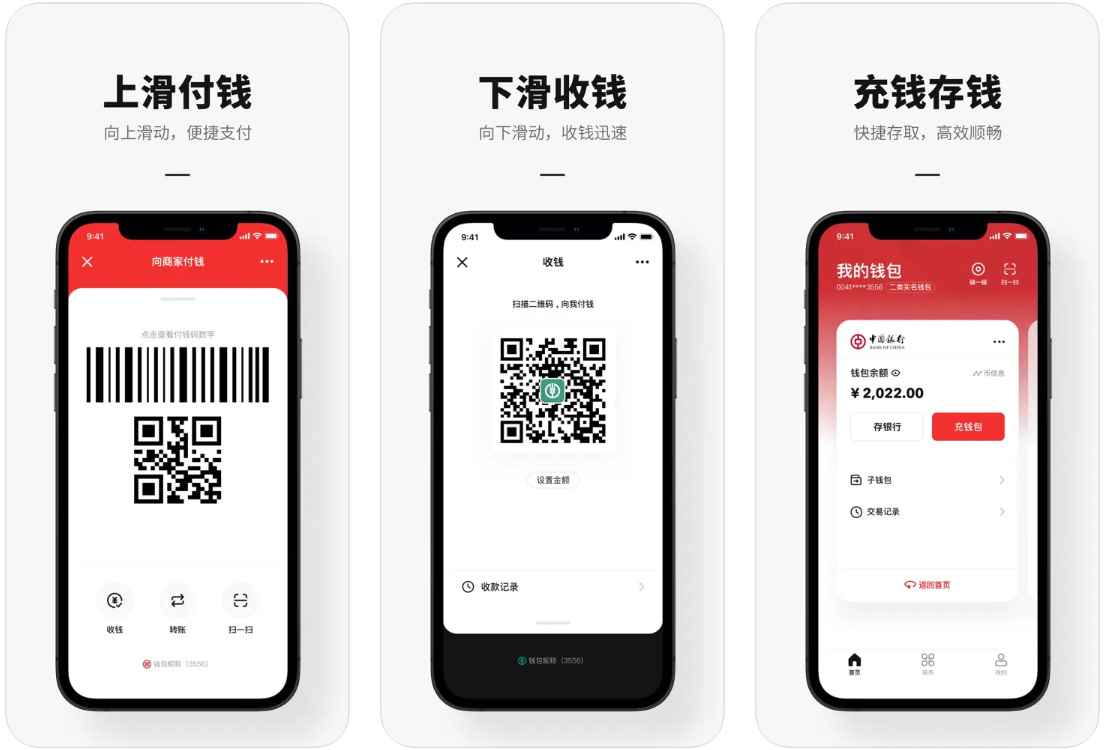

The e-CNY is accessible directly through the e-CNY app, and major private mobile wallet applications AliPay (MyBank) and WeChat Pay (WeBank) where users simply transact through the app with their e-CNY.

Currently in it’s early stages, the e-CNY app/Digital Yuan app does not carry as many privacy violations as apps like AliPay, and WeChat Pay. However, it does not mean it is supporting anonymity and privacy in a place like China. Largest incentive for using the e-CNY app for transactions are not having to pay transaction fees or additional costs for individuals or businesses.

Here is a a quick video to see what it is like to use the e-CNY and it’s payment app.

e-CNY approved Wallet Features:

Physical card contains fingerprint scanner

Apps contain biometric data authorizations

QR Code scanning for spending and receiving

Transaction tracking

Geolocation tracking

Surveillance

CBDCs clearly bring a massive level of invasiveness. It is no surprise the level of oversight and authority the Central Banks have on transaction processing. As transactions settle in real time and the biometric data authorizations are used to approve payments, locations, and the rest of the data is stored and received by the Central Bank.

CBDC wallet features are daunting and scary, but in reality adopting the technology will not be as difficult as some perceive. The psychological barrier isn’t any more than one already experiences by using Apple Pay. Perhaps the biometric data that large social media companies have been storing wouldn’t be a large psychological barrier to climb either?

Apple Pay currently has almost half of the mobile payment market share in the US, 43.9% to be exact, and 500 million users globally. AliPay and WeChat Pay are the largest mobile payment applications in China, and are approved wallets for the e-CNY. AliPay originally introduced it’s mobile e-wallet app in 2008, and 5 years later in 2013 WeChat Pay was introduced. Both of which have employed biometric processing for years - meaning none of these payment is unfamiliar to anyone. Tencent’s WeChat has over 1.2 billion users, 750 million of which are daily users.

Generally if you were to ask anyone who is familiar with CBDC the common response comes in the form of fearing Digital ID’s, social credit scores, and restrictions of public access all integrated with a CBDC. All examples that are found in China on a regular basis. Ironically, you can’t find anything negatively said about the e-CNY from Chinese citizens (it’s probably nothing). Considering there’s no interest paid on holdings in e-CNY accounts

Recent Concerns Across the Globe

Hopefully people don’t believe a central bank is going to allow a token based system where users can find ways to remain anonymous. Surveillance, “security” is the focus. Anonymity is antithetical to the entire point of a CBDC. As with the examples above, CBDCs will be more of an account based system where Digital ID integrations will be the fundamental layer.

Over the last few years you can see why people are scared of CBDCs. Not only because everything is 100% trackable back to the central bank. Many can already see what it’s like to live in a country like China with a surveillance state. Social credit system, digital health passes, digital ID integrations, and biometric authentication for payments.

China

Below is a personal account from a Chinese journalist. Each of the issues listed below come with CBDCs. Make a mistake in a world where everything you do is being traced back to one central account brings forward implications like this:

Liu Hu is a journalist in China, writing about censorship and government corruption. Because of his work, Liu has been arrested and fined — and blacklisted. Liu found he was named on a List of Dishonest Persons Subject to Enforcement by the Supreme People's Court as "not qualified" to buy a plane ticket, and banned from travelling some train lines, buying property, or taking out a loan.

"There was no file, no police warrant, no official advance notification. They just cut me off from the things I was once entitled to," he told The Globe and Mail. "What's really scary is there's nothing you can do about it. You can report to no one. You are stuck in the middle of nowhere."

(Source)

Canada

Back in February Canadian Prime Minister (Dictator) Justin Trudeau and the Canadian government enacted the Emergencies Act to fight off protestors. The government stepped in to assert their powers and extend oversight after a large number of donations were provided to the protestors of the Freedom Convoy.

The restrictions were a massive breach of freedom on Canadian citizens. It allowed for the temporary termination of financial services to any accounts suspected with supporting trucker led blockades, and urged financial institutions to report suspected accounts, and suspend accounts without notice.

Russia

Much like Russia being removed from major global financial systems earlier this year. Russian citizens effectively removed from the global financial system overnight. Some who fled having their assets seized at the border. It’s hard to cover these examples and not to see the massive use case for crypto.

What it Means for You

Think of yourself as a Chinese citizen. You have already been using mobile payment applications for years, for some it is over 10 years. How you transact, who you transact with, how much you spend, your patterns, where you are, what you like, what you support, your plans, and more have been stored with the largest tech companies that the government accesses on a regular basis.

The citizens are under constant surveillance. WiFi sniffers, cameras everywhere, and biometric data is constantly sent back to the government and it’s institutions.

Autist Note: Know full and well this level of surveillance isn’t isolated to China as we all saw from the 2013 NSA leak from Snowden. The NSA collects over 1.7 billion emails, phone calls, and other types of communication on a daily basis and stores them across over a hundred different databases.

(Source)

Now, the Central Bank is coming after all that data and is planning to replace physical cash. They have also banned the use of cryptocurrencies like Bitcoin. All of it is about financial tracking and censorship.

CBDCs can prevent certain activity because they’re digital and do not require anything like a serial number for tracking. Cryptography and a public ledger operated by a central bank creates a simple opportunity to track money throughout their jurisdiction. This creates a scenario where preventing certain transactions using CBDCs is simple. Red flagging transactions, individuals, or business(es) is very easy. We can already see through many instances of censorship today online.

Your ID and all your private data is going to the central bank for constant analysis. All you need to transact with someone is a QR code or P2P, but you know that “up the chain” everything you’re doing is being watched on a whole new level and your transactions can be prevented in the blink of an eye.

So, do you use it? Many are going to say yes, especially if they were a recipient to one of the lotteries/airdrops. Inevitably as a citizen you’re going to use it anyways, right? The Central Bank and the government announced that it plans to move to the e-CNY as the nation’s primary method of payment in the long term. It’s still only in pilot across 23 of the largest cities, and 1 in 5 adults are already using it.

Wrapping Up

If you read up on CBDCs from the rest of the central banks, like with the Sand Dollar and the e-CNY, you’re going to find they all have the same motivations as China and the Bahamas. Tracking and controlling you, your money, and removing any and all privacy.

During the middle of the lockdowns, Summer 2020, only 35 countries were even deciding, whether or not, to develop or launch a CBDC. Now, over 80% of all central banks are active in developing a CBDC - making up over 95% of global GDP.

Nigeria is the last country lately to launch a CBDC (e - Naira).

The two applications for the eNaira are called the speed wallet and the merchant wallet, which are available to download on most app stores. Ironically, the CBDC was originally supposed to be launched on Nigerian Independence Day (Oct 1, 2021), but was pushed back to October 25.

The central banks all have the same talking points, and they all recite the same “initiatives” for developing a CBDC. Best to be listening and developing your multiple income streams as fast as you can.

Don’t eat the bugs!

Anyway to delay or even stop this?

Thanks, good recap